Digital Twin ($21-29B in 2025, CAGR 35-48%) and Physical AI ($5.1-5.4B in 2025, CAGR 31-34%) are each independently fast-growing massive markets. A notable point is that the Digital Twin market is roughly 4x the size of Physical AI. This reflects a structural relationship: Digital Twin is already an operational infrastructure deeply embedded in manufacturing, energy, and construction, while Physical AI is a next-generation technology that must operate on top of that infrastructure.

The core finding of this report is that the two markets are rapidly converging, and a strategic gap exists at their intersection. The cross-market segment of "Digital Twin-based AI Data Infrastructure" is projected to create a $20-40B opportunity by 2030. However, a "Quality Layer" that diagnoses and certifies the quality of synthetic data at this intersection is absent from the global market.

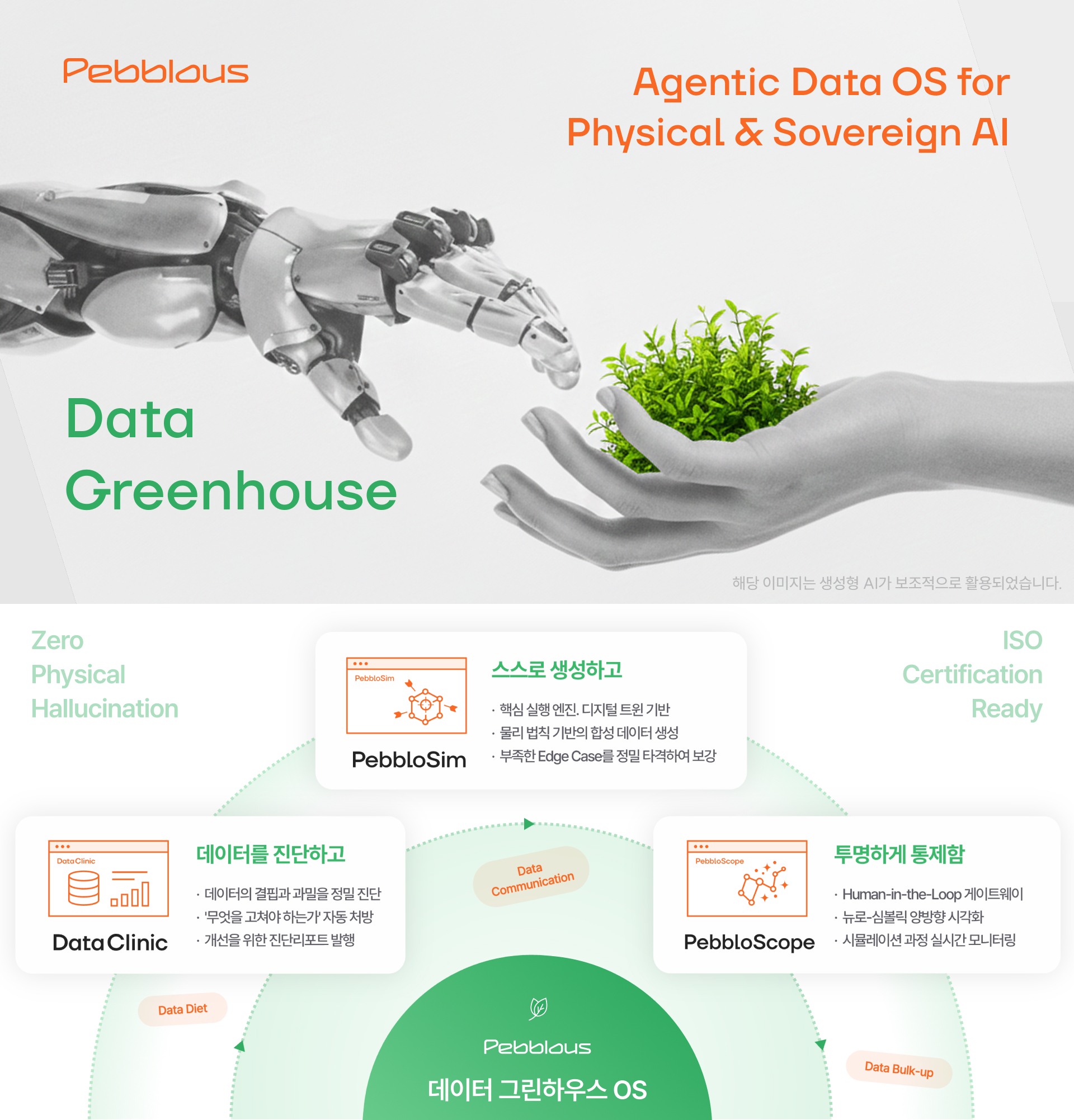

Pebblous targets this structural gap with an integrated platform combining Data Greenhouse (Data OS) + Data Clinic (Quality Assessment) + PebbloSim (Simulation Generation). Aligned with the Korean government's 2026 pan-government AI budget of approximately KRW 10 trillion, MOTIE's M.AX program at KRW 1.0455 trillion (+52% YoY), and the EU AI Act's requirement to demonstrate synthetic data quality, a structure is forming where regulatory compliance capability becomes a market entry barrier.

Digital Twin: The Industrial Nervous System Growing from $21B to $150B

A Digital Twin is a real-time virtual replica of physical assets, processes, and systems. Synchronized with real-world data through sensors and IoT, this virtual model has evolved beyond simple 3D visualization into the digital nervous system of industry, enabling simulation, prediction, and optimization. Predicting factory equipment failures, virtually commissioning new production lines before physical construction, and optimizing energy consumption across entire cities are already reality.

Market Size and Growth

The Digital Twin market is approximately $21-29B in 2025, with projections reaching $122-150B by 2030 (CAGR 32-48%) depending on the research firm. This is roughly 4-5x the size of the Physical AI market ($5.1-5.4B), representing a substantial share even compared to the overall AI market.

The table below compares Digital Twin market forecasts from four leading global research firms. While their scoping methodologies differ, there is a clear consensus on a $1,200B+ market by 2030, with CAGR rates of 32–48% making it one of the fastest-growing segments in the AI industry.

| Firm | 2025 | 2030 Forecast | CAGR |

|---|---|---|---|

| MarketsandMarkets | $21.1B | $149.8B | 47.9% |

| Grand View Research | $25.0B | $155.8B | 34.2% |

| Business Research Co. | - | $122.2B | 32.4% |

| Allied Market Research | - | $125.7B | 39.5% |

The key application area is Predictive Maintenance, which holds the largest share. By industry, Automotive & Transportation (17-32% share) and Manufacturing are leading. On-premise deployment currently dominates, but cloud-based solutions are growing fastest. By region, North America (31-35%) leads, while Asia-Pacific is recording the highest growth rate.

Key Players

The Digital Twin market is dominated by large industrial automation companies.

Siemens

At CES 2026, Siemens announced an "Industrial AI OS" partnership with NVIDIA and launched the Digital Twin Composer. It is converting PepsiCo's U.S. plants into high-fidelity digital twins, and plans to transform its Erlangen, Germany factory into the world's first fully AI-driven adaptive manufacturing facility starting in 2026.

NVIDIA

Provides physics-based simulation and real-time rendering infrastructure through its Omniverse platform. Rather than selling digital twin solutions directly, NVIDIA employs an infrastructure layer strategy where partners like Siemens, Bentley, and Dassault build on top.

Other Major Companies

Dassault Systemes (3DEXPERIENCE), PTC (ThingWorx), Bentley Systems, ANSYS, ABB, GE Digital, and Rockwell Automation compete across design, simulation, and operations domains.

Physical AI: Next-Generation AI Leaping from $5.1B to $50B+

Physical AI, unlike traditional AI that exists only in software, refers to AI that perceives, reasons about, and acts in the physical world. It is embedded in machines with physical bodies -- robots, autonomous vehicles, drones, surgical robots -- that interact with the real world. NVIDIA CEO Jensen Huang declared at CES 2026 that "the ChatGPT moment for robotics has arrived," defining Physical AI as the next great frontier of AI.

Market Size and Growth

The Physical AI market is approximately $5.1-5.4B in 2025. While still in its early stage compared to Digital Twin, explosive growth to $50-84B by 2033-2035 (CAGR 31-34%) is projected.

The table below compares Physical AI market forecasts from three research firms. Unlike Digital Twin, market definitions are not yet standardized, resulting in wider variance. However, the CAGR of 31–34% shows consistent consensus, indicating this early-stage market could grow more than 10x over the next decade.

| Firm | 2025 | 2033-35 Forecast | CAGR |

|---|---|---|---|

| Cervicorn Consulting | $5.13B | $68.5B (2034) | 33.5% |

| SNS Insider | $5.23B | $49.7B (2033) | 32.5% |

| Acumen Research | $5.13B | $83.6B (2035) | 34.4% |

By industry, Manufacturing & Automotive dominates at 45.2%, and by technology, Computer Vision (42-45%) is the core. By form factor, Industrial Robots (36%) are the largest segment, but Collaborative Robots (Cobots) are growing fastest (CAGR 35%). North America leads with a 41% share, while Asia-Pacific (CAGR 33.5%) is growing fastest.

Key Players

Physical AI is a multi-layered arena where AI infrastructure, robotics, and automotive companies compete fiercely.

NVIDIA

Aims to become the "Android for robotics" through Cosmos (World Foundation Model), GR00T (Humanoid AI), Isaac (Robotics Simulation), and Alpamayo (Autonomous Driving).

Tesla

Developing the Optimus humanoid robot through a vertically integrated approach, with a target of producing 100,000 units by the end of 2026.

Boston Dynamics (Hyundai)

Publicly demonstrated the Atlas humanoid for the first time at CES 2026, announcing plans to deploy it in Hyundai's EV factories by 2028.

Google DeepMind

Unveiled the Gemini Robotics model, developing a general-purpose robot AI that performs tasks in physical environments following natural language commands.

Digital Twin x Physical AI: Inevitable Convergence and Explosive Opportunity

Scale Asymmetry: Why Digital Twin Is 4x the Size of Physical AI

The Digital Twin market ($21-29B) is roughly 4x the size of the Physical AI market ($5.1-5.4B). This asymmetry is not merely a numerical difference but reflects the maturity and value chain structure differences between the two markets. Digital Twin is already an operational infrastructure deeply embedded in traditional industries like manufacturing, energy, and construction, while Physical AI is still a next-generation technology in the early stages of commercialization. In other words, Physical AI must operate on the massive infrastructure that Digital Twin has already laid down -- and this is what creates the structural inevitability of convergence between the two markets.

Mapping the key sub-segments of each market makes it clear where the intersections occur.

| Digital Twin Sub-Segment | Share | Physical AI Sub-Segment | Share | Intersection |

|---|---|---|---|---|

| Automotive & Transportation | 17-32% | Manufacturing & Automotive (Industrial/Cobots) | 45.2% | Core Intersection -- Robot motion simulation & synthetic data training on virtual production lines |

| Predictive Maintenance | Largest | Computer Vision (Defect Detection & Environment Perception) | 42-45% | Core Intersection -- DT sensor data + AI vision combined for autonomous inspection & maintenance |

| Energy & Utilities | Growing | Industrial Robots & Drones | 36% | Intersection -- Drone & robot path simulation in hazardous environment DTs |

| Construction & Infrastructure (BIM/Smart City) | Growing | Autonomous Mobile Robots (AMR) | Growing | Partial Intersection -- Autonomous equipment path planning in construction site DTs |

| Healthcare | CAGR ~53% | Surgical Robots & Exoskeletons | CAGR ~35% | Partial Intersection -- Surgery simulation based on patient DTs |

| Aerospace & Defense | 10-15% | Military Drones & Autonomous Vehicles | Growing | Core Intersection -- Autonomous system training in battlefield environment simulation |

It is significant that three core intersection areas (Automotive & Manufacturing, Predictive Maintenance & Vision, Aerospace & Defense) represent the largest segments in both markets. What these intersection areas commonly require is precisely "simulation-based high-quality synthetic data" and "a system to diagnose and certify the quality of that data." This is the reality of the market that Pebblous is targeting.

Why the Two Markets Must Inevitably Meet

The biggest bottleneck for Physical AI is data. Autonomous vehicles need data on wet-road accidents, factory robots need data on part collisions, and military drones need data on nighttime infiltration -- but edge case data like this is nearly impossible to intentionally collect in the real world. This is the "Data Famine" problem.

Digital Twin is the most promising solution to this problem. In virtual environments where physics is precisely implemented, infinitely varied scenarios can be simulated, producing synthetic data immediately usable for AI training at massive scale.

Digital Twin -> Synthetic Data Generation -> Physical AI Training -> Real-World Deployment

This pipeline has already become the core strategy of global leading companies.

NVIDIA

Jensen Huang declared that "digital twins are transforming from passive simulations into active intelligence for the physical world."

Siemens

Building an Industrial AI OS with NVIDIA based on digital twins that "simulates in the virtual world and automates operations in the physical world."

PepsiCo

Converted U.S. plants to digital twins using Siemens Digital Twin Composer, where AI agents run thousands of simulations to derive optimal designs, achieving 90% pre-discovery of potential problems before physical construction.

Convergence Market Size

The intersection of the two markets -- "Digital Twin-based Physical AI Data Infrastructure" -- does not yet have independent market estimates, but its scale can be estimated through aggregation and cross-analysis of multiple market data points.

| Period | Estimated Market Size | Basis |

|---|---|---|

| 2025 | $3-5B | Synthetic data ($0.5-0.9B) + partial DT simulation & optimization segment |

| 2030 | $20-40B | Synthetic data ($2.5-3.4B) + DT-AI integration + partial PAI software layer |

There are three reasons this intersection area is growing rapidly.

First, as regulations like the EU AI Act require proof of synthetic data quality, demand is surging for integrated solutions that encompass "diagnosis-generation-verification-certification" rather than tools that only generate data.

Second, Digital Twin-based simulation is effectively the only methodology for safety verification of Physical AI.

Third, the Korean government's simultaneous investments in Physical AI, AI factories (MOTIE M.AX at KRW 1.0455 trillion, pan-government AI at approx. KRW 10 trillion), smart manufacturing, and digital twins are accelerating policy-driven convergence.

Pebblous Strategy and Opportunity: Structural Advantage Through "Integration"

The Market Gap

Currently, no company in the global market has integrated "data quality diagnosis + Digital Twin-based synthetic data generation + governance audit trails" into a single platform. NVIDIA provides infrastructure but lacks quality assessment and data governance. Siemens is strong in industrial software but has no AI data quality management capabilities. Applied Intuition specializes in autonomous driving and is not a general-purpose Data OS.

Pebblous's Three Pillars

Pebblous targets this structural gap with three products.

Data Greenhouse (Data OS)

A data operating system that executes an autonomous cycle of observation, judgment, action, and certification. It layers on top of existing platforms (Snowflake, Databricks, Data Lake) without replacing them, using a neuro-symbolic diagnostic architecture that combines embedding spaces and ontologies to automatically detect data overcrowding, gaps, and biases.

Data Clinic (Quality Assessment)

An AI data quality assessment engine that diagnoses over 100,000 images per hour. Already validated at Hyundai Motor and Hanwha Vision, it automatically generates quality characteristic mapping based on ISO/IEC 5259 and audit logs at the ISO 42001 level. Pebblous holds quantitative evidence that adding just 5% synthetic data improves AI model performance by approximately 2%.

PebbloSim (Simulation-Based Synthetic Data Generation)

A platform that generates synthetic data for Physical AI on top of digital twin engines. Three key differentiators:

- Vector-to-Param Inverse Mapping: Automatically converts the vector coordinates of data gaps detected by Data Clinic into simulation parameters, generating only the needed data through precision targeting

- Neuro-Symbolic Hybrid World Model: Combines physics-based simulation (symbolic) with generative AI (neural) to guarantee high-quality data free from physical hallucination

- Operational Evidence Package: Records the entire process of why and on what basis data was generated as auditable records, embedding EU AI Act and ISO 42001 regulatory compliance from the design stage

The diagram below illustrates Data Greenhouse's autonomous loop architecture. Built on top of existing data platforms (Snowflake, Databricks, etc.), this system autonomously executes the Observe → Diagnose → Act → Prove cycle. When the neuro-symbolic diagnostics — combining embedding spaces with ontology — detect data density gaps, sparsity, or bias, PebbloSim generates the needed data with precision, and the entire process is recorded as auditable evidence.

Competitive Advantage Comparison

To validate Pebblous' differentiation, we evaluated major competitors across six core capabilities required at the Digital Twin × Physical AI intersection: physics simulation, AI data quality diagnostics, synthetic data generation, data OS, regulatory compliance evidence, and most critically, automated diagnosis-to-generation linkage. As the table below shows, no single player currently covers all six — this is precisely the structural gap that Pebblous targets.

| Capability | NVIDIA | Siemens | Applied Intuition | Pebblous |

|---|---|---|---|---|

| Physics Simulation | ● | ● | ● | — |

| AI Data Quality Diagnosis | — | — | △ | ● |

| Synthetic Data Generation | ● | △ | ● | ○ |

| Data OS & Management | ● | △ | ● | △ |

| Regulatory Compliance Audit Package | — | — | △ | △ |

| Diagnosis-to-Generation Auto-Link | — | — | — | ○ |

● Available · △ Partial · ○ Development Target · — Absent | Applied Intuition's physics simulation is specialized for the autonomous vehicle (AV) domain

Reference Product Lines

The following table details how each company implements the capabilities above through their product suites. NVIDIA provides the infrastructure layer via Omniverse and Cosmos, while Siemens builds the industrial platform with Xcelerator and Digital Twin Composer. Applied Intuition offers the AV-specialized ADAS Toolchain. Pebblous' three products — Data Greenhouse, Data Clinic, and PebbloSim — form an integrated "diagnose-generate-validate-prove" pipeline that no competitor's product suite can replicate.

| Company | Key Products |

|---|---|

| NVIDIA | Omniverse (Simulation), Cosmos (World Model), Nucleus (Data Management) |

| Siemens | Xcelerator (Industrial Platform), Digital Twin Composer, Teamcenter |

| Applied Intuition | ADAS Toolchain, Simian (Simulation), Chassis (Data Management) |

| Pebblous | Data Greenhouse (Data OS), Data Clinic (Quality Diagnosis), PebbloSim (Synthetic Data) |

Strategic Opportunities and Considerations

Opportunity 1: Entering as the "Quality Layer" for Digital Twin

The Digital Twin market ($21-29B) is large, but solutions that guarantee the quality of synthetic data generated within it are absent. Pebblous can position itself to provide a "data quality assurance + regulatory audit trail" layer on top of digital twin infrastructure from companies like Siemens and NVIDIA.

Opportunity 2: Partnering in Korean Manufacturing's Physical AI Transformation

The Korean government's KRW 402.2B Physical AI budget, Hyundai-Boston Dynamics' humanoid robot strategy, HD Hyundai's autonomous vessels, and Hanwha's defense AI investments all require "high-quality synthetic data." Pebblous has already built trust as a data partner to these companies.

Opportunity 3: Building a Competitive Moat Through Data Flywheel

The virtuous cycle where Data Clinic's diagnostic data improves PebbloSim's generation quality, and improved data further enhances diagnostic precision, forms a structural moat that becomes increasingly difficult for competitors to replicate over time.

Considerations

The sim-to-real gap (20-35%), neuro-symbolic technology maturity, and transitioning from government-funded projects to commercial revenue are key risks. The cases of Datagen (shut down after raising $70M) and Synthesis AI (effectively defunct) prove that single-modality synthetic data alone cannot sustain a business -- making Pebblous's integrated platform strategy all the more important.

Conclusion

Digital Twin ($21-29B) and Physical AI ($5.1-5.4B) are massive markets growing at CAGR 35-48% and 31-34% respectively, and their intersection -- "Digital Twin-based AI Data Infrastructure" -- is projected to create a $20-40B opportunity by 2030.

No player in the global market has integrated "diagnosis-generation-verification-certification" at this intersection, and Pebblous's Data Greenhouse + Data Clinic + PebbloSim strategy precisely targets this structural gap.

Korea's strong manufacturing base and government investment in Physical AI provide the optimal foundation for executing this strategy. No player currently exists that integrates "Data OS + Quality Assessment + Simulation Generation" into a single platform -- and this is the essence of the structural opportunity that Pebblous holds.

Frequently Asked Questions (FAQ)

What is the size and growth outlook for the Digital Twin market?

The Digital Twin market is approximately $21-29B in 2025, with growth projections reaching $122-150B by 2030 (CAGR 32-48%). Automotive & Transportation holds 17-32% share as the largest industry, and Predictive Maintenance is the largest application area. North America leads at 31-35%, while Asia-Pacific is recording the highest growth rate.

What are the key growth drivers of the Physical AI market?

The Physical AI market grows from approximately $5.1-5.4B in 2025 to $50-84B by 2033-2035 (CAGR 31-34%). Manufacturing & Automotive dominates at 45.2%, with Computer Vision (42-45%) as the core technology. Collaborative Robots (Cobots) are growing fastest at CAGR 35%.

Why are the two markets converging?

Digital Twin solves Physical AI's biggest bottleneck: data. Edge case data needed by autonomous vehicles, robots, and drones is nearly impossible to collect in the real world, and Digital Twin-based simulation is effectively the only solution. The NVIDIA-Siemens partnership and PepsiCo's digital twin conversion (pre-discovering 90% of potential problems) are already making this convergence a reality.

What is the size of the cross-market opportunity?

The Digital Twin-based Physical AI data infrastructure market is projected to grow from $3-5B in 2025 to $20-40B by 2030. Growth is accelerated by the EU AI Act's synthetic data quality certification requirements, Physical AI safety verification needs, and the Korean government's policy-driven convergence.

What is Pebblous's Three Pillars strategy?

An integrated platform of Data Greenhouse (Data OS), Data Clinic (Quality Assessment), and PebbloSim (Simulation Generation). Key differentiators include diagnosis-to-generation auto-linking that precision-targets data gaps via Vector-to-Param inverse mapping, a neuro-symbolic hybrid world model that prevents physical hallucination, and an operational evidence package for EU AI Act and ISO 42001 compliance.

How does Pebblous differentiate from competitors?

NVIDIA focuses on the infrastructure layer, lacking quality assessment and data governance. Siemens is strong in industrial software but has no AI data quality management capabilities. Applied Intuition specializes in autonomous driving. No integrated player offering "diagnosis-to-generation auto-linking" currently exists in the global market.

What are the key risks and considerations?

The sim-to-real gap (20-35%), neuro-symbolic technology maturity, and transitioning from government-funded projects to commercial revenue are key risks. The cases of Datagen (shut down after raising $70M) and Synthesis AI (effectively defunct) prove that single-modality synthetic data alone cannot sustain a viable business.