Executive Summary

On May 27, 2026, Robinhood formally opened two features that let an AI agent buy and sell stocks and pay with a credit card on a customer's behalf. Give an external AI like ChatGPT or Claude a natural-language instruction such as "switch me into a higher-yield portfolio," and the agent decides on its own when to buy and sell, then places the orders. It is open to all 27.5 million Robinhood customers. Where AI used to give advice, it now moves the money directly.

The backbone is MCP, the Model Context Protocol. For nearly two years this protocol let code editors read repositories; bolted onto Robinhood's servers, it has become infrastructure that moves actual funds. This is the first large-scale release of agentic AI into regulated finance. Yet Robinhood's terms are explicit: the user bears responsibility for every trade the agent makes, and the company does not supervise or audit the agent. Five months before the launch, FINRA had already drawn a line — the moment AI moves from generating content to taking action, a firm's supervisory duty shifts.

The thread this piece follows is a single question: for an agent to be allowed to move money in a person's place, what state must the data beneath that judgment be in? Walk through what Robinhood opened and how, where it parts ways with robo-advisors, the split that opened across the industry, and the line FINRA drew on liability — and the answer to that question gathers, all of it, as data.

Key Figures

Sources: CNBC, Robinhood Newsroom, FINRA

Four numbers carry the weight of this announcement: the customer base opened to agents, the cashback attached to agent purchases, the lead time by which regulation got ahead of the product, and where liability points. The last number matters most. Autonomy is delegated 100%, but the responsibility for outcomes stays 100% with the user.

27.5M

customers opened to agents

The first large-scale opening of agentic AI into regulated finance

3%

cashback on agent purchases

Earned when the AI pays via the agentic card — a design that rewards autonomous spending

5 months

regulation's head start

FINRA's "Trade Execution Agent" definition (Dec 2025) preceded the launch (May 2026)

100%

user liability

Every agent trade is the user's responsibility; Robinhood does not supervise or audit

What Robinhood Did

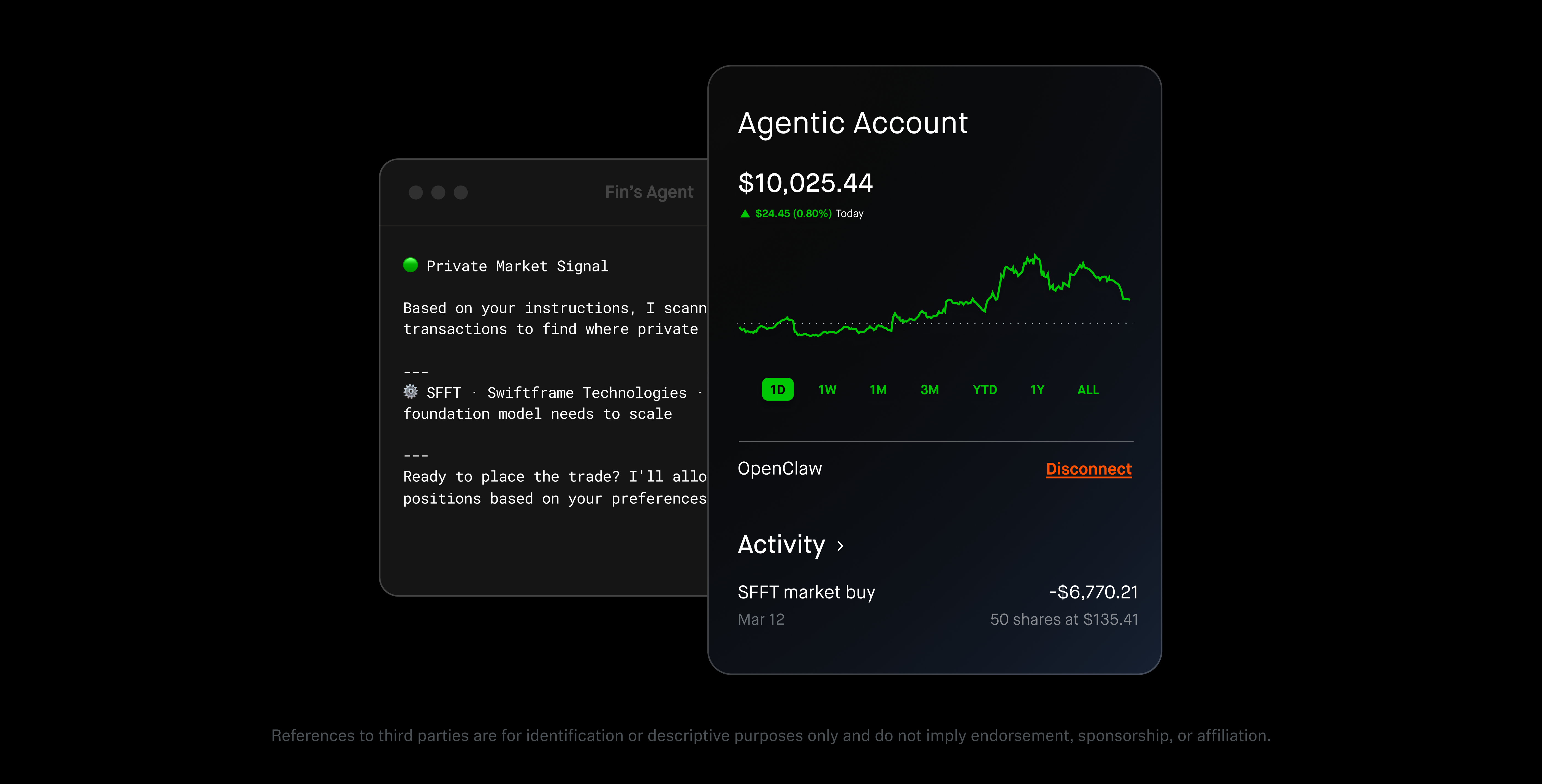

On May 27, 2026, the headline Robinhood ran in its newsroom was "Robinhood is now open to agents." The announcement, covered the same day by CNBC, TechCrunch, and Bloomberg, has two parts. One is agentic trading: a third-party AI agent autonomously buys and sells stocks on the user's behalf. The other is the agentic credit card: an AI agent pays directly through a dedicated virtual card. Founder Vlad Tenev's line captures the nature of the announcement: "Our mission has always been to democratize finance for all, and now that mission extends to AI agents."

This was not a sudden leap. Robinhood released its analysis-and-insight tool, Cortex, first, in March 2025. Cortex only guided; it did not trade. That May an early beta of agentic trading appeared, and a year later — on May 27, 2026 — trading and the credit card went live together. It is a two-tier structure: an execution layer that acts, sitting on top of Cortex, which guides. Advice and execution, once kept apart, are now stitched into one.

The point is simple: AI buys stocks in your place, and swipes the card in your place. The user throws out an intent in natural language — "buy those sneakers if the price drops below a certain line," or "cut the volatility in this portfolio" — and the agent handles the rest. The reason this is an inflection point is that AI, until now, lived in the seat of an advisor that tells you what you might do. Now it goes past advice and pulls the trigger.

What changed: the core shift is from "AI advises" to "AI moves the money directly." The moment trading and payment are handed to an agent, what you need to assign right and wrong is traceability and audit of outcomes. Who placed that order, why, and on what data — that becomes a money question immediately.

MCP Now Moves Money

The technology behind the features is MCP, the Model Context Protocol. An open standard created by Anthropic, it lets an AI agent call external tools through a structured server interface. Robinhood stood up its own MCP server, and the trading endpoint is agent.robinhood.com/mcp/trading. Point an agent client at that address and the connection is done. At launch the supported clients were Claude Code, Claude Desktop, ChatGPT, Codex (OpenAI), Cursor, and Grok, and any other MCP-capable client can connect through the same link.

Here is the change worth naming. For the past two years MCP mostly let code tools read repositories and handle files. The same protocol now moves funds in real accounts. An interface that read code became an interface that moves money — that, precisely, is the technical center of gravity of this event. The standard is unchanged; what the standard touches shifted from text to assets.

2.1Permissions Split Three Ways

Robinhood's documentation divides the permissions given to an agent into three. First, read everywhere: the agent can read positions, balances, portfolio, orders, and trade history across both the regular and the agentic accounts. Second, trade only in the agentic account: order execution is possible only in an isolated "agentic account" the user has funded separately. The agent cannot trade in the main account. Third, research tools: ticker search, real-time quotes, tradability checks, popularity lists, and watchlist management.

- • Account isolation: the agent touches only the funds the user has placed in the agentic account. The assets in the main account stay out of reach.

- • Real-time activity feed: every time a trade happens a push notification arrives, and a preview is shown before an order executes. You can sever the connection instantly with one tap.

- • Authentication on desktop only: after opening the agentic account, agreeing to the terms, transferring funds, and verifying in the mobile app, you paste a local URL into the agent. Permissions come in three modes: allow all, confirm each time, or deny specific ones.

2.2The Card Gives a Limit, Not a Number

The agentic credit card connects the agent to Robinhood Banking's MCP server. At setup a dedicated virtual Robinhood Gold card is issued, and the user sets the spending limit and whether manual approval is required. The crucial design choice is that the card number is never exposed to the agent. What the agent receives is not the card number but a "right to initiate transactions," gated by limit and approval. It gets used to buy sneakers when a price drops below a set line, book a restaurant, or purchase a domain. Agent purchases earn 3% cashback. The feature opens first to existing Robinhood Gold card customers and expands to the Platinum card slated for later this year.

The asset scope is still narrow. In beta the only tradable asset is stocks; options, crypto, event contracts, futures, and prediction markets remain on the roadmap for the second half of 2026. That said, as of mid-2026 the options tools were not yet surfaced in most agent clients — meaning the "AI options trading" marketing runs ahead of the actual tool surface. And for an agent to trade autonomously, a client such as Claude Code has to stay running on the user's computer.

The heart of the design: an isolated account, an unexposed card number, permissions gated by limit and approval. Instead of giving the agent "direct access to money," Robinhood gives it "the right to initiate constrained actions." It is a careful starting line — autonomy allowed inside a controllable boundary.

How It Differs from Robo-Advisors

"AI helps you invest" is not a new story. Betterment and Wealthfront have run robo-advisors that automatically manage portfolios for over a decade, and Charles Schwab's Intelligent Portfolios sit in the same lineage. So it is easy to read Robinhood's announcement as "just another automated-investing feature." But the operating principle is fundamentally different.

A robo-advisor is a fixed algorithm. It takes in the user's risk profile and rebalances on a schedule according to predetermined asset-allocation rules. What to adjust, when, and how is baked into code written by a human. Algorithmic trading is the same: code implementing a specific strategy simply reacts to signals. Agentic trading, by contrast, takes a natural-language intent and has a general-purpose LLM generate a judgment on the spot. Given the same "reduce my volatility" instruction, which stocks to sell and when is decided by the agent reading real-time context.

| Dimension | Robo-advisor · algo trading | Agentic trading |

|---|---|---|

| Decision-making | Fixed rules / strategy code written by humans | General-purpose LLM generates judgments from real-time context |

| Input | Risk profile and parameter settings | Natural-language intent ("boost my returns") |

| Scope of action | Rebalancing within a fixed asset set | Stock selection, timing, and order placement all delegated |

| Predictability | High (rules are explicit) | Low (the same instruction can yield different outcomes) |

| Audit difficulty | Low (read the code) | High (multi-step reasoning is hard to trace) |

That difference becomes the new risk directly. When a fixed rule produces a bad outcome, you can point to the code and find where it went wrong. But an LLM agent's judgment can take a different path each time on the same instruction, and reconstructing that reasoning after the fact is far harder. The more autonomy grows, the trickier it becomes to retrace what decided the action.

An Industry Split in Two

Right after Robinhood's announcement the industry split clearly into two camps. On one side are the execution-first players that hand the agent the act itself. Robinhood opened the door with its isolated-account model, and Interactive Brokers introduced agentic trading via Claude in June 2026. Public.com also runs AI agents for investing. On the other side are the assistive-and-traditional players. Charles Schwab released an AI insight feature that explains portfolio performance and market activity, but the human does the trading. The robo-advisors at Betterment and Wealthfront still sit in rule-based automated management.

Even within the execution camp the grain differs. Interactive Brokers chose an enterprise-integration approach that needs no separate account and shares no credentials. Robinhood chose the opposite — an isolated-account model where the user sets aside funds separately. The former lays an agent over the existing account to add convenience; the latter weighs toward fencing the risk inside a wall. Inside the same sentence, "the agent trades," the way trust is designed splits like this.

What's notable is that the assistive camp does not deny the demand itself. In Schwab's survey, more than 60% of investors showed interest in AI-powered features. The market wants AI to come deeper into investing. What splits opinion is "how far do you delegate?" — to advice, or all the way to execution. This boundary is likely to be the competitive axis of fintech for the next several years.

The axis of competition: the industry split not over "will we use AI" but over "will we hand the agent execution." And even among those who chose to delegate execution, how the risk is fenced (isolated account vs. enterprise integration) becomes the differentiator. In the end the crux is what structure you design trust in.

Who's Liable — the Line FINRA Drew

Robinhood's terms make the location of liability clear: the user bears responsibility for every trade the agent executes. The terms do not pass liability to the agent or the model provider. In its disclaimers the company wrote that "AI agents can make errors, misinterpret instructions, and act in unexpected ways," and stated that it does not control, supervise, monitor, recommend, or audit the agent. On top of that, the moment data passes to the AI provider the user has chosen, it leaves Robinhood's secure environment and falls under that provider's terms.

Yet the regulator had already drawn a line from another direction. In its 2026 Annual Regulatory Oversight Report, published on December 9, 2025, FINRA took agentic AI head-on — about five months ahead of the launch. The report named a category, the "Trade Execution Agent": an autonomous system that performs market analysis, strategy generation, and trade execution under varying levels of human oversight. And it set a core principle: the moment AI goes beyond generating content to acting, a firm's supervisory, recordkeeping, and governance duties shift in substance.

FINRA pointed to six risks: autonomy that acts without human verification, deviation beyond the granted scope and permissions, limits on auditability and transparency that make multi-step reasoning hard to trace, data sensitivity, lack of domain knowledge, and poorly designed reward functions. The controls the regulator expects of firms are equally clear: monitor the agent's system access and data handling, define human-in-the-loop procedures, log actions and decisions, and set guardrails that constrain behavior. It also nailed down a warning against inflated AI marketing — so-called "AI washing."

Here a tension appears. Robinhood chose a structure of "we provide only the infrastructure, the liability is the user's," while FINRA says "when AI that acts appears, the firm's supervisory duty grows." How far Robinhood, as a broker-dealer, carries supervisory responsibility, and how suitability or best-execution obligations apply to an inappropriate order placed by an agent, remain an unsettled gray zone. A direct read from the SEC on whether existing rules fit unattended investment judgment is not yet visible either.

The line that was drawn: Robinhood placed liability with the user; FINRA saw the supervisory duty pointing toward the firm. Where the two positions meet there is a shared demand — log the actions, make them traceable, set guardrails. Translate that demand into technology, and it becomes, in the end, a question of how you handle data.

Data Is the Guardrail

The risks FINRA listed all come back to data. Auditability is the question of "can we retrace what data the agent looked at to place that order?" Lack of domain knowledge is the question of "is the market data the agent referenced accurate in that context?", and data sensitivity is the question of "where does the portfolio and trade history flow, and under whose terms does it land?" The quality of an agent's judgment cannot exceed the reliability of the data that judgment rests on. Wrong or biased market data leads straight to real losses and mistaken payments.

So for agentic finance AI to be trusted, the data beneath it has to be in a trustworthy state first. Three things are preconditions.

- • Traceable data provenance: a record of what data the agent fetched, when, and from where, and used in its judgment. When a trade is disputed later, audit only holds if the basis for the action can be reconstructed.

- • Verified real-time market data: the accuracy and timeliness of quote, fill, and availability data must be guaranteed. A contaminated input spreads straight into a wrong order.

- • Governance of permission and leakage: which data flows to which agent and provider, and whether consent and constraints are placed along that path, must be managed. It is about controlling the moment data leaves the secure environment.

Robinhood's safeguards — account isolation, the activity feed, order previews, instant disconnection — are all meaningful guardrails. But these are a fence around the agent's actions. The guardrail over the input that produces those actions — the quality and provenance of the data — has been passed off to the model provider the user chose. That is why a fence around the input matters as much as a fence around the action. If the data cannot be trusted, no matter how tight the constraints on behavior, they cannot stop a wrong judgment itself.

The core proposition: the more an agent's autonomy grows, the more the center of gravity of trust moves from the model to the data. Only data with traceable provenance, verified market feeds, and permission-and-leakage governance can make an agent's actions auditable. In that sense, data is the agent's last guardrail.

Beyond Finance, Into Other Verticals

The Robinhood case is not a story that stays inside finance. A structure where an agent takes hard-to-reverse actions in a person's place, with responsibility attached to the result, is a pattern other regulated industries will soon meet. In healthcare an agent suggests a prescription or books an appointment; in law it executes contract terms; in education it automatically adjusts a learning path. The domains differ, but the skeleton of the design is the same: isolated permissions, human-in-the-loop, action logging, a clear liability structure, and verified data.

Finance does have a particularity it hit before other verticals. Trades are hard to reverse, and markets move in real time. The cost of a wrong judgment shows up immediately and quantitatively. So the trial and error finance passes through first becomes a kind of trailer for the verticals that follow. Where liability turns ambiguous, what data enters a judgment unverified, what logs are needed after the fact — finance will show all of it first.

This is also where the reason Pebblous has focused on making data AI-Ready connects. Once an agent starts acting rather than merely advising, the reliability of that action is determined by the source, quality, and provenance of the input data. Robinhood's announcement shows that this shift is no longer an abstract forecast but a reality unfolding across 27.5 million accounts. The next question is clear: before deciding what to delegate to an agent, have you made the data that will hold up its judgment trustworthy first?

Closing: Robinhood opened, at scale and for the first time, the authority for AI to move money. Autonomy was delegated but liability stayed with the user, and what can fill the gap between them is only traceable, verified data. In the age of agents, the first asset to check is not a smarter model but data you can trust to act on.

References

Official Documents

- 1.Robinhood Newsroom. (2026). "Robinhood is now open to agents." Robinhood. — Official launch of agentic trading and the credit card; Tenev's remarks.

- 2.Robinhood Support. (2026). "Agentic Trading overview." Robinhood. — MCP endpoint, the three permissions, authentication flow, safeguards.

- 3.Robinhood. (2026). "Agentic Trading on Robinhood | Safe AI Trading Agents." Robinhood. — Supported platforms, isolated account, asset-scope roadmap.

- 4.FINRA. (2025). "2026 Annual Regulatory Oversight Report." FINRA. — Trade Execution Agent definition, the six risks, expected controls.

- 5.FINRA Blog. (2026). "Emerging Trend in GenAI: Observations on AI Agents." FINRA. — Acting AI and the principle of the supervisory-duty shift.

Industry & Press

- 6.CNBC. (2026). "Your AI agent can now trade for you on Robinhood. And buy stuff with your credit card too." CNBC. — 27.5M customers, overview of the two products.

- 7.TechCrunch. (2026). "Robinhood now lets your AI agents trade stocks." TechCrunch. — How to connect over MCP, supported clients.

- 8.Bloomberg. (2026). "Robinhood Unveils AI Agents for Stock Trading, Credit Card Purchases." Bloomberg. — Launch context and market reaction.

- 9.Decrypt. (2026). "Robinhood Opens Platform to AI Agents for Stock Trading and Credit Card Spending." Decrypt. — Card virtual-number, limit, and cashback design.

- 10.FinTech Global. (2026). "Interactive Brokers launches agentic trading via Claude." FinTech Global. — Enterprise integration vs. isolated account comparison.

- 11.Charles Schwab Pressroom. (2026). "Charles Schwab Launches AI-Powered Capability...." Charles Schwab. — Assistive AI insights, investor-interest survey.

- 12.Public.com. (2026). "AI Agents for Investing." Public.com. — A comparable case from the execution camp.